Our Ranking

Our proprietary investment analysis system is able to rank the 1200 companies I keep in our database according to several factors. These factors lead us to six ranks based upon traditional investment concepts: Earnings Growth, Financial Strength, Value, Momentum, Quality and Fundamentals. Each of the rankings combines several financial ratios that reflect each of the above investment concepts, and they are chosen based upon years of analysis that show that these specific ratios provide me with a clear picture of how the company fairs under each concept. They are ranked from 100 (best) to 1 (worst) on a relative basis to their industry and to the S&P 1500.

Companies Ranked as Candidates For Investment

In the first four entries in this series, we looked at Quality Ranked companies , Earnings Growth Ranked companies, Financial Strength Ranked companies, and Fundamental Ranked companies. Today, we are going to look at companies to see if they are Candidates For Investment based upon aggregating the four ranking systems.

Over the years, I have found that when a company ranks highly on all four of the ranking systems, they are a strong candidate for further due diligence to see if they make the cut to be included in client portfolios.

Below are a selection of companies from our database with a rank above 90 on each of the four ranking systems and a history of above average bear market performance plus those with a rank below 60 on each of the ranking systems and a history of very weak bear market performance.

| Company Name | Quality Rank | Earnings Growth Rank | Financial Strength Rank | Fundamental Rank | 3-yr Avg Return |

|---|---|---|---|---|---|

|

Avery Dennison Corp |

98.4 |

96.3 |

93.8 |

92.3 |

29% |

|

Cabot Oil & Gas Corp |

97.8 |

95.2 |

99.4 |

95.1 |

-9% |

|

Jazz Pharmaceuticals PLC |

98.6 |

95.1 |

91.1 |

95.6 |

1% |

|

Mercury General Corp |

92.9 |

94.6 |

98.7 |

98.1 |

14% |

|

NVR Inc |

99.9 |

98.2 |

97.7 |

93.6 |

17% |

|

Rio Tinto PLC |

96.5 |

95 |

94.1 |

99.9 |

23% |

|

Southern Copper Corp |

91.5 |

98.3 |

93.6 |

95.6 |

16% |

|

The Toro Co |

92.4 |

93 |

92.6 |

94.7 |

25% |

|

Werner Enterprises Inc |

90.2 |

96.1 |

94.3 |

97 |

10% |

|

Winnebago Industries Inc |

98.3 |

99.6 |

98 |

94.2 |

28% |

|

Aurora Cannabis Inc |

41.7 |

10 |

9.6 |

22.3 |

-50% |

|

Altisource Portfolio Solutions SA |

31 |

4.7 |

13.1 |

27.2 |

-38% |

|

Coty Inc |

20 |

50.2 |

32.1 |

32.8 |

-9% |

|

FuelCell Energy Inc |

24.7 |

25.6 |

21.1 |

27.2 |

-24% |

|

Fluor Corp |

49.2 |

30.4 |

49.1 |

59.9 |

-25% |

|

The Howard Hughes Corp |

40.8 |

37.8 |

20.9 |

43.8 |

-6% |

|

Norwegian Cruise Line Holdings Ltd |

|

10.2 |

3.1 |

17.1 |

-15% |

|

Ocean Power Technologies Inc |

59 |

29.4 |

11.8 |

10.8 |

-52% |

|

PBF Energy Inc |

30.2 |

59.2 |

36.2 |

49.8 |

-27% |

|

Low Growth |

Limoneira Co |

32.2 |

-7% |

||

|

Spirit AeroSystems Holdings Inc |

40.2 |

13.1 |

14.8 |

38.5 |

-16% |

|

Triumph Group Inc |

34.8 |

43.1 |

45.2 |

44.3 |

-2% |

|

Tata Motors Ltd |

22 |

41.7 |

34.4 |

46 |

1% |

|

T2 Biosystems Inc |

22 |

48 |

35 |

6.8 |

-46% |

|

AgEagle Aerial Systems Inc |

9.4 |

30.1 |

11.5 |

15.3 |

31% |

|

Alkaline Water Co Inc |

26.4 |

29.1 |

13.7 |

17 |

-7% |

|

Wynn Resorts Ltd |

32.9 |

16.3 |

13 |

33.2 |

-10% |

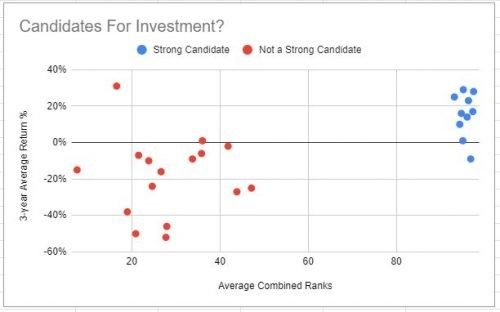

A review of the chart above will indicate that the companies highly ranked performed better on average over the past three years than those ranked low. So, lets look at the scatter graph for a visual analysis:

Looking at the graph, it is easy to conclude that the companies ranked highly on all four ranking systems have materially out-performed those with low ranks on all four ranking systems on average over the past three years.

Why Is This Important Now?

In the first entry in this series, I mentioned that the Federal Reserve had begun to discuss tightening monetary policy, an event that has in the past led to stock market corrections and sometimes full bear markets. Given their recent statements, it is prudent to know how companies will perform when there is not a significant stimulus pushing their stock prices higher.

Investment Strategy

In the normal course of portfolio management during this period in time where we have been warned that monetary tightening is in the plans, we want to book the gains on the companies that show the least ability to withstand a bear market and focus on the companies that have the best ability to withstand a bear market. We do not want to see the gains we have made be lost by not monetizing them when the market tells us it is time.

What’s Next?

We have looked at the combined ranks on a 3-year average return comparison so lets look at it on a 10-year average return comparison to make sure the correlation between high ranks and high returns holds true.

-Mark