Our Ranking

Quality Ranked Companies

Today, I thought we would look at our Quality Rank – one of the factors that lead to their being designated as High Quality or Low Quality. The other factors include having 9 of past 10 years as profitable, a Return on Invested Capital > Weighted Average Cost of Capital, Growing Book Value, growing earnings, bear market stock price performance, etc.

However, being either high or low quality in and of itself is not a reason to buy or sell a company – there are times in the market that High Quality companies under-perform Low Quality companies,and visa versa. No one set of ratios can tell you everything you need to know to buy or sell a company, but it gives you a place to start due diligence that gets you to the buy or sell decision.

Starting with our Quality Rank, this set of ratios gives me a feel for the soundness of a company’s financial position. The ratios I use are centered around four major items that comprise quality: Gross and Operating Margins; Asset Turnover; ROE and ROI; and Debt Management.

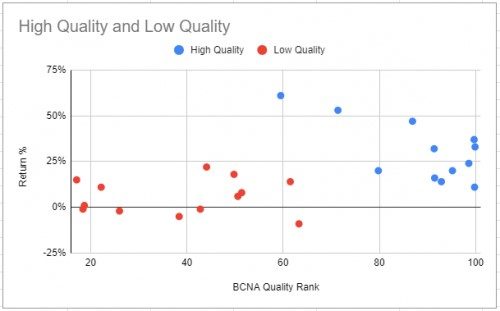

Below is a non-exhaustive list of companies from our database that are categorized as either High Quality or Low Quality.

| Quality | Company Name | BCNA Quality Rank | 3yr Avg Return |

|---|---|---|---|

|

Low Quality |

Alaska Air Group Inc |

50.6 |

6% |

|

Low Quality |

Bank of America Corp |

17.1 |

15% |

|

Low Quality |

Cornerstone Building Brand |

42.8 |

-1% |

|

Low Quality |

Chevron Corp |

18.4 |

-1% |

|

Low Quality |

Ford Motor Co |

22.2 |

11% |

|

Low Quality |

Fifth Third Bancorp |

61.5 |

14% |

|

Low Quality |

General Electric Co |

18.7 |

1% |

|

Low Quality |

JPMorgan Chase & Co |

49.8 |

18% |

|

Low Quality |

Truist Financial Corp |

51.4 |

8% |

|

Low Quality |

Valero Energy Corp |

63.3 |

-9% |

|

Low Quality |

WESCO International Inc |

44.1 |

22% |

|

Low Quality |

Wells Fargo & Co |

26 |

-2% |

|

Low Quality |

Exxon Mobil Corp |

38.4 |

-5% |

|

High Quality |

Dollar General Corp |

91.4 |

32% |

|

High Quality |

Genmab A/S |

99.7 |

37% |

|

High Quality |

Barrick Gold Corp |

98.6 |

24% |

|

High Quality |

Kirkland Lake Gold Ltd |

99.9 |

33% |

|

High Quality |

Mercury General Corp |

92.9 |

14% |

|

High Quality |

Boston Beer Co Inc |

59.5 |

61% |

|

High Quality |

Southern Copper Corp |

91.5 |

16% |

|

High Quality |

Skyworks Solutions Inc |

79.8 |

20% |

|

High Quality |

Taiwan Semiconductor |

86.9 |

47% |

|

High Quality |

UnitedHealth Group Inc |

95.2 |

20% |

|

High Quality |

Veeva Systems Inc |

71.4 |

53% |

|

High Quality |

Vertex Pharmaceuticals Inc |

99.8 |

11% |

This scatter plot makes it easy to see that the Blue Dots representing the High Quality companies are well above (i.e., higher three year average return) the Red Dots representing Low Quality companies. Again, let me restate this: Low Quality does not mean they are bad, it just mean that in the three most recent years the ratios that define them as Low Quality were not as high as other companies in their industry or in the S&P 1500.

Why Is This Important Now?

Investment Strategy

What’s Next?

Our next discussion will be on our Earnings Growth Rank – the original analytical system whose nexus started with my Masters Thesis that set out to disprove the Efficient Market Hypothesis (yes, that is how long ago it was – it has graduated to a Theory and is no longer a Hypothesis). The synopsis of the thesis was that in spite of the strong support for the Hypothesis, there really are certain financial ratios in the public realm that when viewed as a whole can provide index beating returns over the long run. And given our track record of beating the index over the long run, the Earnings Growth Rank is a very important part of our investment process.

-Mark