Investing in the AIPositioning for Technological Transformation (2025-2040)

Investing in the AI Revolution will be key to portfolio performance as it is the most important economic force of our time. It’s changing industries, job markets, and the flow of money faster than ever before. Artificial Intelligence has moved from being just an idea to actually making things more efficient, creating new infrastructure needs, and opening up opportunities for wealth creation that will continue to grow until 2040.

But this change isn’t happening in isolation. It’s being influenced by larger economic factors like America’s debt crisis, which presents serious challenges to our financial future. The national debt is expected to surpass $50 trillion in the next ten years, a situation that could significantly impact how investments are made. To understand this issue better, check out our in-depth analysis on America’s debt crisis.

This post is the first in a series explaining the varied parts of the AI Revolution and provides you with background on why our blog post on the data center gold rush was just the beginning of the many investment opportunities that are available to diversify a portfolio, yet maintain a focus on this secular change to how we will live life in the future and that will drive portfolio returns to market-beating results.

Will it be a straight line up? Definitely not – there will corrections along the way, even bear markets with significant losses along the way – but with a long investment horizon (I’m using 2040 for this series) this will be the most transformative technology since the internet came to be.

Why Understanding Investment in AI Requires More than Data Centers

Knowing how to invest in the AI revolution goes beyond just finding popular stocks. To make smart investment decisions, we need to look at the bigger picture and understand how different industries are connected. This includes the obvious sectors like semiconductors and data centers, as well as energy infrastructure such as Nuclear Energy Generation, Natural Gas Production, and Gas Turbine Generators that support computing needs. But I believe the AI Revolution will progress in four phases and today’s focus on data centers will evolve to the impact on end users’ increasing margins and productivity from needing fewer people to

Practical Investment Guidance

This article aims to provide practical guidance for investors and financial experts on Investing in the AI Revolution over the next 15 years. Here’s what you can expect:

- Insights into the macroeconomic factors influencing investments in technological transformation

- Exploration of specific opportunities within the AI ecosystem

- Examination of infrastructure requirements driving parallel investments in power generation

- Analysis of workforce and educational trends affecting long-term returns

Additionally, it’s crucial to understand how events like the tariff conflict can cause disruptions in financial markets, impacting investor sentiment and capital allocation.

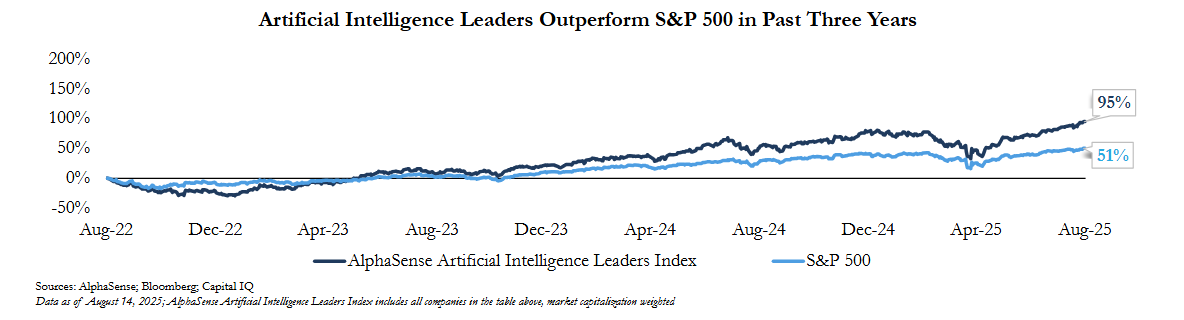

Our Data Center focus has been very profitable for client portfolios so far. By preparing strategically today for future phases of the AI Revolution, , we can position our portfolios to benefit from the fundamental changes that Artificial Intelligence will bring to the global economy.

Graph From: https://www.ropesgray.com/en/insights/alerts/2025/08/artificial-intelligence-h1-2025-global-report

The Macroeconomic Context Impacting AI Investment

The Federal Reserve’s monetary policy stance shapes the foundation for Investing in the AI Revolution through 2040. Recent Federal Reserve rate cut decisions signal a shift from the aggressive tightening cycle that characterized 2022-2023, creating a more favorable environment for capital-intensive technology investments. The central bank’s pivot reflects confidence in moderating inflation impact while supporting continued economic growth through strategic rate adjustments.

AI-driven productivity gains present a compelling counterbalance to traditional economic headwinds. Economists project GDP expansion of 2.5-3.2% annually through 2030, with artificial intelligence contributing an estimated 1.2 percentage points to this growth. This productivity surge occurs even as workforce displacement accelerates, demonstrating AI’s capacity to generate economic value beyond simple labor substitution.

Interest rate dynamics directly influence capital allocation decisions across sectors:

- Technology sector valuations become more attractive as borrowing costs stabilize between 3.5-4.5%

- Infrastructure investments gain momentum with predictable financing costs supporting long-term project planning

- Risk premium compression in growth stocks creates entry points for strategic positioning

The relationship between inflation expectations and Investing in the AI Revolution remains particularly relevant. As AI technologies reduce production costs across industries, they exert deflationary pressure on goods and services while simultaneously requiring substantial upfront capital deployment. This dynamic creates a unique investment landscape where patient capital positioned in AI infrastructure stands to benefit from both technological advancement and favorable monetary conditions.

For further insights into these trends and their implications on various sectors, consider subscribing to Mark’s Investment Blog, where we tackle such topics.

AI Adoption: Disruption and Opportunity in Employment and Productivity

The rapid rise of AI adoption brings both challenges and opportunities for the American workforce. According to current projections, 30-40% of jobs are expected to be affected by workforce displacement by 2040, with the rate of displacement increasing from about 2% per year in 2025 to 4-5% per year by the mid-2030s. This sharp increase is a result of the widespread use of large language models, computer vision systems, and robotic process automation across various industries.

This will become a big issue when we get to Phase Two of the AI Revolution – the mass adoption phase. Investing in the AI Revolution will focus on companies that are expanding their profit margins and productivity by replacing humans with AI and robots. There may also be an investment opportunity beyond what I have shown below for private education companies that focus on skills retraining. That we won’t really know until we approach Phase Two.

Jobs at High Risk of Automation

Some job categories are more vulnerable to automation than others. Here are some examples:

- High Risk (85%+ probability): Data entry clerks, telemarketers, basic bookkeeping positions

- Moderate Risk (70-80% probability): Customer service representatives, paralegal assistants, retail cashiers

- Significant Impact: The financial services sector is expected to undergo major changes as roles like traditional analysts are replaced by algorithmic trading, automated underwriting, and AI-driven portfolio management.

According to recent industry surveys, over 60% of executives cite workforce retraining as the single most critical factor for successful AI adoption—surpassing even technology investment itself. As displaced workers transition into positions that demand proficiency with artificial intelligence, we will see a complex employment dynamic develop.

Employment Dynamic

- Short-Term Productivity Gains: Companies adopting AI technologies often experience immediate improvements in operational efficiency—commonly reporting productivity boosts between 20% and 35%. These gains are typically realized in areas such as automated data processing, streamlined decision-making, and the reduction of manual errors. As the adoption curve steepens, these gains will become more widespread and accepted as the norm.

- Uneven Distribution of Benefits: While AI-driven automation delivers substantial productivity gains, the advantages are not shared equally across all segments of the workforce or industries.

- Highly digitalized fields—such as technology, finance, and healthcare—are poised to reap outsized rewards, whereas traditional sectors like manufacturing or agriculture may experience slower growth and fewer immediate benefits.

- Employees with advanced technical skills or strong adaptability often gain access to higher-paying, AI-augmented roles.

- In contrast, workers in routine or repetitive jobs face a greater risk of displacement without equivalent opportunities for advancement. This will likely lead to a higher level of structural unemployment

- Urban centers with robust tech infrastructure will attract more investment and job creation from AI initiatives, leaving rural areas that are slower to adopt AI at risk of being left behind.

- Organizational Divide: Larger companies have the resources to implement comprehensive AI strategies and upskilling programs sooner rather than later. Small and medium-sized businesses may lack the capital or expertise to fully participate in—and benefit from—the automation revolution. New industries that cater to them will likely develop that provide access to automation on a contractual basis.

- Challenges for Organizations: Many firms encounter obstacles during AI rollouts, including: Resistance to change among legacy staff; increased demands for ongoing technical training; and difficulties in aligning existing business processes with new automation platforms.

Category A Companies: Primary Beneficiaries of Investing in the AI Revolution

1. Data Centers and Infrastructure: The Backbone of the AI Economy

The physical infrastructure supporting artificial intelligence represents a generational investment opportunity spanning the next 15 years. As AI models grow exponentially in complexity and computational requirements, the demand for sophisticated data center facilities has reached unprecedented levels.

The Growing Demand for Data Centers

Global data center capital expenditure is projected to surge dramatically through 2040, with industry analysts forecasting investments exceeding $500 billion annually by the decade’s end. This massive capital deployment reflects the fundamental reality that every AI application—from autonomous vehicles to medical diagnostics—requires substantial computing power housed in specialized facilities. A prime example of this trend is the $500 Billion Stargate Project, which is revolutionizing data center infrastructure through AI integration and advanced cooling technologies.

The Power Behind Hyperscale Data Centers

Hyperscale data centers’ power demand presents particularly compelling investment dynamics. The United States alone faces a thirtyfold increase in power consumption from AI-related computing infrastructure by 2040. Current estimates suggest AI workloads will consume approximately 8% of total US electricity generation within this timeframe, compared to less than 0.3% today.

Data Center and Infrastructure Investment Strategies for the AI Revolution

Investing in the AI Revolution through data center exposure includes several strategic approaches:

- Direct ownership of data center REITs and operators

- Real estate developers in areas close to energy sources

- Infrastructure development companies specializing in facility construction

- Semiconductors and server providers capable of processing data far beyond what we have today

- Cooling and power management technology providers

- Fiber optic and networking equipment manufacturers

- Energy Utilities – Natural Gas, Nuclear, Hydroelectric (where available) will dominate, but Hydrogen is on the rise

- Energy Infrastructure withing Data Centers – Small Nuclear Reactors and Gas Turbine Generators

The data center gold rush is reshaping real estate, energy, and technology markets, presenting numerous emerging opportunities at the intersection of AI, cloud computing, and infrastructure development.

The Complex Needs of Data Centers

Data centers require not just physical space but sophisticated cooling systems, redundant power supplies, and advanced networking capabilities. Companies positioned at the intersection of these requirements stand to capture significant value as the AI economy expands.

2. Semiconductor Industry: Driving Force Behind AI Hardware Innovation

The growth of the semiconductor market presents compelling investment opportunities as artificial intelligence applications require increasingly advanced processing capabilities. Advanced chip manufacturers specializing in AI-optimized designs should receive significant portfolio allocation, with recommended weightings between 15-25% for growth-oriented investors seeking exposure to this technological transformation.

The Importance of GPU Manufacturing in AI Hardware Innovation

GPU manufacturing plays a crucial role in AI hardware innovation. Market projections indicate that this industry will grow from $65 billion in 2024 to approximately $280 billion by 2032, representing a compound annual growth rate exceeding 20%. This growth is driven by the increasing computational needs for:

- Training and inference operations of large language models

- Real-time computer vision processing in autonomous systems

- High-performance computing clusters supporting scientific research

- Deployment of edge AI across consumer electronics and industrial equipment

Barriers to Entry in AI Chip Production

The specialized nature of AI chip production creates significant barriers to entry, resulting in market share being concentrated among established players with advanced manufacturing capabilities. Companies that lead in producing chips with 3-nanometer and smaller process nodes command premium valuations justified by their technological advantages and capacity constraints that shows demand outstripping supply.

Impact of AI Infrastructure Buildout on Memory and Storage Semiconductors

The memory and storage segments of the semiconductor industry also stand to benefit from the expansion of AI infrastructure. This is because training datasets and model parameters require exponentially larger storage capacity. Within the broader semiconductor ecosystem, high-bandwidth memory technologies specifically designed for AI accelerators represent a secondary investment consideration.

3. Energy Sector Transformation Supporting AI Infrastructure Growth

The exponential growth of AI computing demands creates unprecedented pressure on power generation capacity.

Nuclear Energy

Nuclear energy data centers represent a critical infrastructure solution as traditional power grids struggle to meet the intensive electricity requirements of large-scale AI operations. Major technology companies are already securing dedicated power sources for their facilities, recognizing that energy availability will determine competitive positioning through 2040.

Small Nuclear Reactors (SMRs) emerge as the preferred technology for powering next-generation data centers. These modular units deliver 50-300 megawatts of carbon-free baseload power directly to facilities, eliminating transmission losses and grid dependency. Companies like NuScale Power and TerraPower are advancing commercial deployments, with regulatory approvals accelerating throughout 2024-2025.

Potential Investment Opportunities in Nuclear

Investing in the AI Revolution will span the nuclear energy supply chain:

- Uranium mining and enrichment companies positioned for sustained demand growth

- SMR developers and engineering firms specializing in modular reactor design

- Nuclear fuel cycle service providers

- Utilities partnering with tech companies on dedicated nuclear installations

The convergence of AI infrastructure needs with carbon reduction mandates creates a multi-decade tailwind for nuclear energy investment, particularly in technologies purpose-built for data center applications.

Natural Gas

The rapid growth of AI computing is driving a comeback in high-efficiency natural gas power generation. As large AI data centers put pressure on local energy grids, having dedicated gas power plants—either on-site or nearby—provides a quick and flexible solution to meet the massive energy demands of AI facilities until 2040.

Leading companies in the industry are looking into long-term power purchase agreements linked to new gas power plants. This is because having immediate access to energy, the ability to adjust power output quickly, and shorter construction timelines (usually between 18 to 36 months) can greatly influence where data centers are built and how competitive they are in the market.

Modern gas turbine technologies fit this need perfectly. Simple-cycle turbines can be set up quickly to provide large blocks of power (ranging from 50 to over 300 megawatts) with fast start times and the ability to ramp up power output quickly during peak AI usage periods. Combined-cycle plants, on the other hand, use heat-recovery steam generators to increase overall efficiency (up to around 58% to 64%) and reduce emissions per unit of electricity generated.

To ensure a reliable energy supply, infrastructure such as dedicated gas pipelines, backup liquefied natural gas (LNG) facilities, and on-site gas storage are being developed. Additionally, newer turbine models are designed to accommodate hydrogen fuel (typically in blends ranging from 20% to 50% by volume) as a way to future-proof against regulations aimed at reducing carbon emissions.

The lifecycle emissions associated with natural gas can further be minimized through various measures such as carbon capture retrofits, blending renewable natural gas (RNG) into the fuel mix, and implementing strategies to prevent methane leaks throughout the entire supply chain.

Potential Investment Opportunities in Natural Gas

There are several areas within the natural gas and turbine ecosystem that present potential investment opportunities:

- Upstream producers and LNG exporters who have the ability to provide long-term firm contracts.

- Midstream operators involved in pipeline transportation and storage facilities that enable dedicated fuel delivery.

- Original equipment manufacturers (OEMs) and suppliers of key components used in heavy-duty turbines, heat-recovery steam generators (HRSGs), compressors, and control systems such as GE Vernova, Siemens Energy, and Mitsubishi Power.

- Engineering, procurement, and construction (EPC) firms along with developers specializing in fast-track projects involving simple-cycle and combined-cycle power plants. Additionally, providers of long-term service agreements (LTSA) also play a crucial role.

- Companies focused on carbon management solutions, renewable natural gas (RNG) initiatives, and hydrogen-blend infrastructure that enhance the lifespan of existing assets while ensuring compliance with environmental regulations.

The combination of constant energy demand from AI applications and the need for quick-to-install, scalable solutions creates favorable conditions for natural gas-powered generation tied specifically to data centers.

Hydrogen Power

More and more energy companies, manufacturers, and large tech companies believe that hydrogen can help them produce enough electricity in the future while also reducing their carbon emissions. Here’s how it works:

- Production: Hydrogen can be made in different ways, such as using natural gas with carbon capture technology or by splitting water molecules using renewable energy sources like wind or solar power.

- Storage: Once produced, hydrogen can be stored in various forms such as underground salt caverns, high-pressure tanks, or as a liquid.

- Conversion: When needed, hydrogen can be converted back into electricity using specially designed gas turbines or fuel cells.

This process is particularly beneficial for AI data centers because it provides a flexible energy solution that can:

- Support renewable energy sources like wind and solar by filling in the gaps when they’re not producing enough power

- Replace diesel backup generators with cleaner technology

- Provide backup power for extended periods without relying solely on the electrical grid

Immediate Benefits

In the short term, existing gas power plants can reduce their carbon emissions by blending hydrogen into their fuel mix (usually around 20-50% hydrogen) without completely replacing their infrastructure. This gradual transition aligns with the growing demand for cleaner energy solutions.

Long-Term Potential

Over time, we can expect to see dedicated hydrogen turbines and large-scale fuel cell installations providing reliable power generation with minimal environmental impact. These technologies have the potential for quick start-up times, high ramp rates (ability to adjust power output quickly), and reduced local air pollution.

Turning Waste Energy Into Fuel

By combining on-site hydrogen production through electrolysis with excess wind or solar energy generation, we can convert otherwise wasted energy into storable fuel. This means that even when renewable sources are not actively generating power, we can still rely on them to produce hydrogen and meet our energy needs.

Overcoming Challenges

While there are still obstacles to overcome—such as high costs, efficiency losses during energy conversion processes (known as round-trip efficiency), and the need for new infrastructure development—the path forward is clear: hydrogen has the potential to enhance our energy systems.

Potential Investment Opportunities in Hydrogen

Here are some areas where we see potential for investment across the hydrogen power sector:

Electrolyzer manufacturers, infrastructure, and suppliers:

Companies producing equipment used in green hydrogen production such as PEM (Proton Exchange Membrane), alkaline, or solid oxide electrolyzers.

-

- Plug Power (PLUG), Bloom Energy (BE), Cummins/Accelera (CMI), Nel ASA (NEL.OL), ITM Power (ITM.L), ThyssenKrupp Nucera (NCH2.DE): PEM/alkaline/SOEC electrolyzers, stacks, and systems for data-center-adjacent H₂.

- Bloom Energy (BE), Ballard Power (BLDP), FuelCell Energy (FCEL), Doosan Fuel Cell (336260.KS): Stationary fuel-cell systems (SOFC/PEM) for low-emission baseload and UPS/backup replacing diesel gensets.

-

Chart Industries (GTLS): Cryogenic tanks, heat exchangers, liquefaction, and BOP that sit at the heart of H₂ value chains.

-

Hexagon Purus (HPUR.OL), Nikkiso (6376.T): High-pressure storage, transport modules, and cryogenic systems.

-

Vertiv (VRT), Eaton (ETN), Schneider Electric (SU.PA): Power distribution, UPS, and thermal systems; natural fit to integrate fuel cells/H₂ backup into white-space designs.

-

Quanta Services (PWR), Fluor (FLR), KBR (KBR): EPC capacity for electrolyzers, pipelines, and turbine/fuel-cell projects.

Hydrogen-ready turbine and fuel cell manufacturers:

Original Equipment Manufacturers (OEMs) producing turbines and fuel cells designed to run on both natural gas and hydrogen fuel.

-

-

-

GE Vernova (GEV), Siemens Energy (ENR.DE), Mitsubishi Heavy (7011.T): Large-frame turbines certified for H₂ blends today and roadmap to higher shares; key for behind-the-meter power blocks at AI campuses.

-

Baker Hughes (BKR): Turbomachinery, compressors, and process equipment used across H₂ plants and pipelines.

-

-

Midstream/storage developers:

Companies involved in building pipelines, trailers for transporting hydrogen, liquefaction facilities (turning gaseous hydrogen into liquid form), and geological storage sites for storing large quantities of hydrogen.

-

- Enbridge (ENB), TC Energy (TRP), Kinder Morgan (KMI), Williams (WMB): Rights-of-way, compression, and storage assets adaptable to hydrogen blending and future dedicated H₂ service.

Clean hydrogen producers:

Businesses creating blue (produced from fossil fuels with carbon capture) or green (produced from renewable sources) hydrogen along with platforms that facilitate off-taking agreements tied to growing data center energy demands.

-

-

Air Products (APD), Linde (LIN), Air Liquide (AI.PA / AIQUY): Build/operate hydrogen plants, liquefaction, logistics, and long-term supply contracts.

-

CF Industries (CF), Yara (YAR.OL), OCI Global (OCI.AS): Ammonia (a key H₂ carrier) and blue/green ammonia projects tied to power and export hubs.

-

Shell (SHEL), BP (BP), TotalEnergies (TTE), Equinor (EQNR): Integrated energy majors developing large blue/green H₂ hubs and pipelines.

-

Controls/safety/integration providers:

Companies specializing in standardizing deployment at scale through control systems (managing operations), safety measures (ensuring safe handling of gases), and balance-of-plant components (supporting infrastructure like compressors or valves).

-

- Honeywell (HON), Emerson (EMR), Rockwell (ROK): Process control, valves, sensors, and safety systems required across H₂ production, storage, and power conversion.

The Role of Hydrogen in the Energy Mix

When combined with other low-carbon options like nuclear power and natural gas, hydrogen becomes an important part of our future energy landscape—offering an adaptable solution capable of meeting diverse needs while positively impacting pollution. What sets it apart is its ability to be implemented gradually over time—starting with blending existing fuels today before transitioning towards dedicated use tomorrow—making it compatible with evolving timelines associated with AI infrastructure development projects. The percentage of profitability from hydrogen for the companies listed above is not a catalyst to invest in them at this time. However, over the course of our journey to 2040, hydrogen will likely become quite important as an additional source of energy – and potentially a primary source of energy – to power the AI Revolution.

Category A Portfolio Allocation Target Framework

| Sector | 2028 Weight | 2032 Weight | 2036 Weight | 2040 Weight | Rationale |

| Semiconductor/GPU/Memory | 35% | 40% | 45% | 50% | Highest growth; technology leadership |

| Electric Utilities | 20% | 15% | 15% | 15% | Early infrastructure; steady returns |

| Data Center REITs | 20% | 25% | 25% | 20% | Infrastructure demand; consolidation |

| Data Center Infrastructure | 15% | 10% | 10% | 10% | Early buildout; maturation |

| Nuclear & Natural Gas Power Production | 10% | 10% | 5% | 5% | Long-term energy; policy support; reliability |

Risk-Adjusted Return Target Projections (cumulative)

| Investment Tier | 2028 Returns | 2032 Returns | 2036 Returns | 2040 Returns |

| Technology Leaders | 30-45% | 60-80% | 80-120% | 100-150% |

| Infrastructure Providers | 20-35% | 40-60% | 60-90% | 80-120% |

| Utility Operators | 15-25% | 30-50% | 40-70% | 60-90% |

| Supporting Services | 18-28% | 35-55% | 50-80% | 70-100% |

| Nuclear & Natural Gas Specialists | 25-40% | 50-75% | 70-110% | 90-130% |

Category A: AI Investment Timeframes

2028 – Infrastructure Buildout Phase (Core Holdings)

The first wave is all concrete, copper, and compute. Before AI can scale up in size and depth, the world needs a massive expansion of physical capacity: cutting-edge chips (NVDA), advanced manufacturing (TSM), and high-bandwidth memory (SK Hynix, MU) to feed model training and inference. That silicon must live somewhere, so data center landlords (EQIX, DLR) and power providers (CEG nuclear, NEE renewables) become critical bottleneck solvers. Meanwhile, hyperscalers (MSFT, AMZN) integrate the new computing power into cloud stacks and software tooling so enterprises can actually use it. This phase comes first because nothing else happens without power, space, cooling, and chips—these are the gating items the entire stack stands on.

2032 – Enterprise Adoption Phase (Growth Accelerators)

Once capacity is in place, the center of gravity shifts to distribution: getting AI into every workflow, device, and edge node. Platform leaders (NVDA, GOOGL, MSFT) expand ecosystems and software layers; CPU/GPU alternatives (AMD) gain share as enterprises diversify; design enablers (ARM) and equipment leaders (ASML) monetize the ongoing node transitions. At the edge, Qualcomm and Apple push custom silicon into phones, PCs, and wearables, while Broadcom powers networking and accelerators. Vertiv scales thermal and power systems to keep densities rising. This comes second because enterprises only adopt at scale once the cost curves, tooling, and supply chains laid down in 2028 make AI reliable, affordable, and easy to deploy.

2036 – Market Maturation Phase (Consolidation Winners)

With AI embedded across industries, competition concentrates around scale advantages, Intellectual Property depth, and full-stack control. Technology leaders (NVDA) defend their moats with software and silicon lock-in; ecosystem integrators (AAPL, MSFT, GOOGL) capture recurring platform economics; manufacturing gatekeepers (TSM, ASML) exercise pricing power as nodes become more complex; memory remains an oligopoly (SK Hynix, Samsung, MU). Incumbents with geographic and product breadth (INTC) regain relevance in diversified or sovereign supply chains, and global platforms (EQIX) remain indispensable interconnecting hubs. This phase naturally follows adoption: profit pools consolidate as standards have developed and only a handful of players can afford the capex and R&D to stay on the frontier.

2040 – Mature Market Phase (Oligopoly Leaders)

In maturity, AI resembles other networked technologies: a few firms set technical roadmaps and economic terms. NVDA and a small group of processor vendors form an effective oligopoly in the high-end AI computing industry; TSM’s manufacturing dominance and ASML’s tool monopoly make them the ultimate price-setters for progress. Platform owners (AAPL, MSFT, GOOGL) monetize ubiquitous AI services at software-like margins; Micron, Samsung, and SK Hynix control memory supply-demand cycles; ARM continues to license the instruction-set plumbing underneath it all; Intel persists as a strategically important U.S. chip maker and foundry. This end state comes last because markets evolve toward concentration as complexity, capital intensity, and switching costs rise—leaving a durable, slower-changing structure where a few leaders capture most of the value.

Anticipated Category A Winners by Timeframe

2028 Core Holdings (Infrastructure Buildout Phase)

NVIDIA (NVDA) – AI computing dominance

Taiwan Semiconductor (TSM) – Manufacturing leadership

SK Hynix (000660.KS) – HBM market control (private company)

Equinix (EQIX) – Global data center platform

Digital Realty (DLR) – Hyperscale partnerships

NextEra Energy (NEE) – Renewable infrastructure

Constellation Energy (CEG) – Nuclear power

GE Verona (GEV) – Gas Turbine Generators

NuScale Power (SMR) and BWX Technologies (BWXT) – Small Nuclear Reactors

Microsoft (MSFT) – AI software integration

Amazon (AMZN) – Cloud infrastructure

Micron Technology (MU) – Memory expansion

2032 Growth Accelerators (Enterprise Adoption Phase)

NVIDIA (NVDA) – Ecosystem dominance

Qualcomm (QCOM) – Edge AI leadership

Apple (AAPL) – Custom silicon integration

Taiwan Semiconductor (TSM) – Advanced node premium

AMD (AMD) – Enterprise AI expansion

Alphabet (GOOGL) – AI platform integration

Arm Holdings (ARM) – Architecture licensing

ASML (ASML) – Technology enablement

Broadcom (AVGO) – Infrastructure semiconductors

Vertiv (VRT) – Cooling infrastructure

2036 Consolidation Winners (Market Maturation Phase)

NVIDIA (NVDA) – Technology leadership

Apple (AAPL) – Ecosystem integration

Taiwan Semiconductor (TSM) – Manufacturing control

Samsung Electronics (005930.KS) – Vertical integration

Alphabet (GOOGL) – Platform dominance

ASML (ASML) – Equipment monopoly

SK Hynix (000660.KS) – Memory oligopoly (private company)

Microsoft (MSFT) – Software platform

Intel (INTC) – Geographic diversification

Equinix (EQIX) – Global platform

2040 Oligopoly Leaders (Mature Market Phase)

NVIDIA (NVDA) – AI processor oligopoly

Taiwan Semiconductor (TSM) – Manufacturing monopoly

Apple (AAPL) – Platform dominance

Samsung Electronics (005930.KS) – Integrated stack

Microsoft (MSFT) – Recurring revenue

ASML (ASML) – Technology gatekeeper

Alphabet (GOOGL) – AI services platform

SK Hynix (000660.KS) – Memory control (private company)

Arm Holdings (ARM) – Architecture licensing

Intel (INTC) – US technology legacy company

Conclusion

Investing in the AI revolution requires a thoughtful approach that considers multiple interconnected sectors. To make the most of this technological transformation, investors should focus on three key areas:

1. Semiconductor Innovation

Invest in companies that are developing advanced GPU architectures, specialized AI chips, and next-generation fabrication technologies. These innovations are crucial for powering machine learning systems.

2. Data Center Infrastructure

Allocate funds towards real estate investment trusts (REITs), construction firms, and operators who manage the physical facilities where AI computation takes place. This sector is currently experiencing unprecedented demand.

3. Power Generation Technologies

Include investments in nuclear energy solutions, particularly small modular reactor developers and uranium producers. Additionally, consider renewable energy providers who are meeting the growing electricity needs.

To successfully invest in the AI revolution, it’s important to understand that hardware, infrastructure, and energy are all interconnected. Each sector has the potential to enhance the growth of the others. By diversifying your investments across these areas, you can reduce concentration risk while still benefiting from the long-term trends that are reshaping economies worldwide.

Next Time

In Part 2 of this series, I’ll give you the remaining categories in the Sector Analysis along with the Category B, C, and D companies that fit into portfolio positioning.

Thanks for reading the blog!

If you ever need help managing your investments, please contact Vice President Joel Wallace. You can reach him by email at [email protected], or you can call him at (217) 351-2870 to speak directly.